Cost Ch eleven

Personnel Department would be allotted to the Information Systems Department. Personnel Department are allotted solely to the Information Systems Department. Assembly Department are allotted https://cryptolisting.org/blog/how-do-you-allocate-service-department-costs-to-production-departments to the Information Systems Department and the Personnel Department.

Apportionment Of Overhead Expenses:

First, the Definitions and Uses of Cost Allocation and Cost Approtionment. Secondly, assigning acceptable parts of the totals to individual allocation of factory service department costs to the production departments is necessary to: product items, organizations, or events.

Advantages Of Departmentalization Of Overhead Expenses:

Therefore, there could be zero equivalent units with respect to part HH887 in the work in course of inventory at the finish of April. Machining Department would be allocated to the Information Systems Department. Personnel Department could be allocated to the Assembly Department and the Machining Department.

- This methodology does not take into effect the fact that a service department may be providing providers to other service departments too.

- It is the only methodology that totally accounts for the reciprocal provision of services amongst departments.

- Use the direct methodology to allocate support division costs to production departments, and decide the predetermined manufacturing overhead charges for the two production departments.

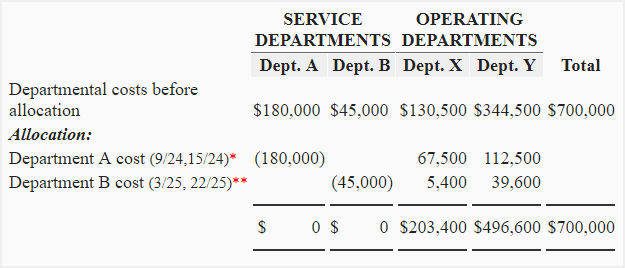

- In the direct method of price allocation, the allocation of the service departments is completed to the production departments.

- As acknowledged in the earlier answer, beneath the reciprocal companies technique the entire support departments’ prices are allotted amongst the entire departments that use the various support departments’ output of services.

- Cost is allocated only to the production or the working departments.

Cost Accountancy

Similarly, the price of repairs and maintenance of a selected machine ought to be charged to that exact department whereby the machine is positioned. Power, if separate meters are offered at every cost centre and fuel oil for boilers are different examples of allocation. So, the time period allocation means the allotment of the whole merchandise without division to a selected department or cost centre. The number of such departments and their quantity will rely upon the character of business, type of labor performed and the dimensions of the manufacturing facility. For instance, in Steel Rolling Mill, Hot Mill, Cold Mill, Pickling Shop, Annealing Shop, Hardening, Polishing and Grinding are the producing departments.

A. Personnel Department would be allocated to the Information Systems Department. C. Personnel Department are allotted solely to the Information Systems Department. costs of the Machining Department are allocated to the Assembly Department. This basis is used for the apportionment of power bills.

ultimately applied by the person departments to the models allocation of factory service department costs to the production departments is necessary to: produced.

If all machines function eight hours a day, to calculate this number, multiply eight hours occasions 5 days every week, then multiply that by fifty two weeks. If two machines function full-time in the machining department and one machine operates full-time in the finishing division, then machine hours equate to 4,a hundred and sixty and a couple of,080 respectively. Product manufacturing ought to be analyzed first from the actions that go into it (for instance, manufacturing machine set up and machinery maintenance). These operations usually happen solely after manufacturing many product models.

Machining costs are $33.65 an hour and finishing prices are $28.eighty five an hour. Find the whole https://cex.io/ period of time every division runs per yr.